A June thunderstorm pushes through Springfield with 65 mph straight-line winds. The next morning you spot shingles in the yard and a section of lifted edges along the south-facing gable. Your first thought: does my insurance cover this? Wind damage roof repair in Springfield, MO is one of the most common post-storm searches for good reason. This guide explains what wind damage looks like, what your policy covers, what it does not, and what steps protect your claim.

TLDR: Standard homeowners insurance covers sudden wind damage to your roof, gutters, and siding. The most common denial reasons are wear and tear, improper installation, and cosmetic damage exclusions. Get a professional inspection before you call your insurer because documentation wins claims. June is the peak month for damaging wind in the Springfield area, and standard shingles are rated right at the severe wind threshold.

Why Springfield Roofs Take So Much Wind Damage

NWS Springfield data confirms that June is the most active month for damaging wind events in the Springfield forecast area. April is a close second. The severe weather season runs April through August, and NWS defines damaging wind as gusts that reach or exceed 58 mph.

That 58 mph number matters. Standard builder-grade shingles carry an ASTM D3161 Class A rating, tested at 60 mph under lab conditions. That leaves very little margin in real storms where gusts, turbulence, and roof shape all affect performance. NOAA data shows Missouri experienced 120 confirmed billion-dollar weather and climate disasters from 1980 to 2024, and 82 of those were severe storm events involving high winds and hail.

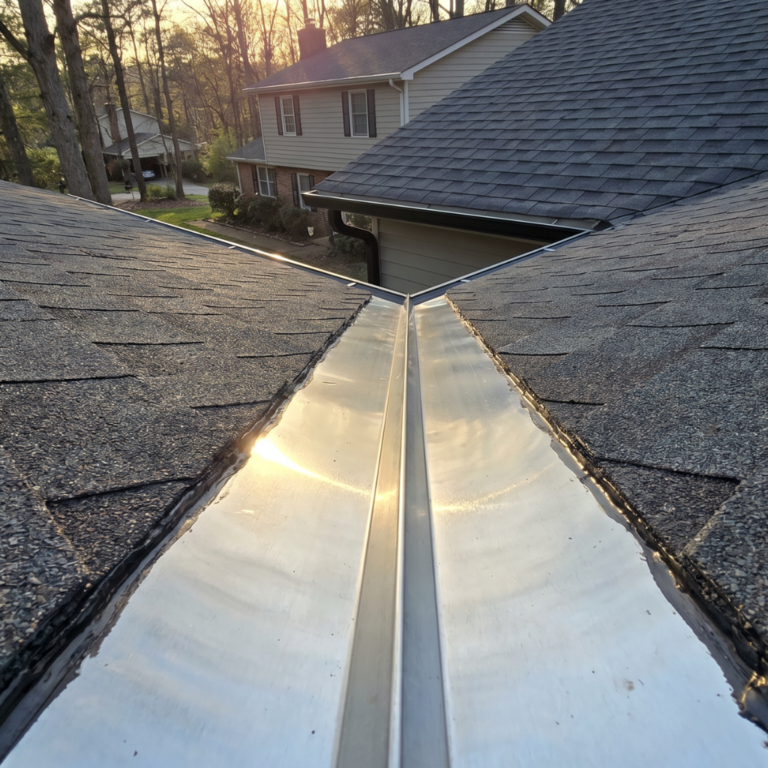

Wind does not hit a roof evenly. It creates uplift pressure, a suction force that is strongest at corners, rake edges (gable ends), eaves (the bottom edge), and the ridge. That is why wind damage almost always starts at the edges of the roof, not the center. Once wind gets under a shingle tab and breaks the adhesive seal, the changed shape of the lifted shingle increases suction even more. One lifted tab leads to the next. It is a chain reaction.

Pro tip: Three-tab shingles are far more vulnerable to wind uplift than architectural (laminated) shingles. If your roof still has three-tab shingles, every storm is a higher risk event.

What Does Wind Damage Look Like on a Roof?

Wind damage is not always obvious from the ground. Here are the seven most common signs.

- Missing or detached shingles with bare underlayment showing through

- Lifted or curled shingle edges where the adhesive seal has broken

- Granule loss concentrated in gutters and at downspout outlets

- Damaged or lifted flashing around chimneys, skylights, and vents

- Cracked or missing ridge cap shingles along the peak of the roof

- Scrapes, punctures, or broken sections from airborne debris

- Visible sagging or bowing where structural decking took uplift damage

Wind does not just damage the roof. The same storm that lifts shingles also pulls gutters off the fascia board, peels siding panels from the bottom edge, and displaces soffit panels. All of that damage belongs on the same insurance claim. Document every exterior surface, not just the roof.

Pro tip: One storm equals one claim. Walk all four sides of your home after a wind event and photograph the roof, gutters, siding, soffit, and fascia. Damage to all of these surfaces from the same storm belongs on the same claim.

What Homeowners Insurance Covers After Wind Damage

Standard homeowners insurance covers sudden wind damage as a named peril. That includes missing shingles, lifted flashing, structural debris impact, and damaged gutters or siding caused by the same storm event. The damage must be sudden and accidental, not pre-existing.

Here is what policies typically cover and what they do not.

| Situation | Covered? | Why |

|---|---|---|

| Missing shingles from last week’s storm | Yes | Sudden wind damage is a named peril |

| Gradual shingle lifting from aging sealant | No | Classified as wear and tear |

| Lifted flashing from a storm event | Yes | Sudden damage to a functional component |

| Gutters pulled off by the same wind | Yes | Same-event damage, same claim |

| Siding panels peeled by the same wind | Yes | Same-event damage, same claim |

| Damage your insurer calls “cosmetic only” | Maybe | Depends on whether your policy has a cosmetic exclusion |

The four most common denial reasons for wind claims are wear and tear, improper installation, lack of maintenance, and missed filing deadlines. The Missouri Department of Commerce and Insurance requires insurers to acknowledge your claim within 10 working days. The 15-day accept/deny window starts after your insurer receives your completed proofs of loss, not from your initial call. Missouri does not set a single statewide filing deadline, so check your specific policy.

The Cosmetic Damage Exclusion

This is the angle most homeowners miss entirely. A cosmetic damage exclusion is a policy clause that excludes coverage for damage that affects only appearance, not function. If your roof sheds water normally despite the damage, the insurer may call it cosmetic and deny the claim.

Functional damage, where the roof’s ability to shed water is reduced or its lifespan is shortened, is still covered even under a cosmetic exclusion policy. The gray area is a wind-lifted shingle with a broken sealant bond that has not caused a leak yet. Is that functional or cosmetic? This is one of the most common adjuster dispute points.

Carriers in high-storm states, including Missouri, are increasingly adding these endorsements at renewal. Check your declarations page for “cosmetic damage exclusion” or “limited cosmetic coverage” language. A professional inspection that documents functional damage, not just visible damage, is the strongest counter to a cosmetic exclusion denial.

Wind Damage: Repair or Replace?

| Factor | Lean Toward Repair | Lean Toward Replacement |

|---|---|---|

| Roof age | Under 10 to 12 years | 15 years or older |

| Damage location | Isolated to one slope | Spread across multiple slopes |

| Repair cost vs. replacement | Under 70% of replacement cost | Over 70% of replacement cost |

| Water intrusion | None present | Active leaks or decking damage |

| Shingle type | Architectural (holds repairs better) | Three-tab (weak sealant, color mismatch) |

If your wind claim results in a full replacement, consider upgrading your shingles. Standard Class A shingles are rated to 60 mph. Architectural shingles carry a Class F rating of 110 mph. Class 4 impact-resistant shingles like Owens Corning Duration FLEX carry a 130 mph manufacturer wind warranty and meet the ASTM D7158 Class H uplift test standard (150 mph). They also add the best hail protection available. For homeowners weighing repair vs. full replacement, a FEMA fact sheet on shingle wind resistance explains why installation method and shingle rating both matter.

Illustrative Scenario

Illustrative scenario: Two homeowners in Battlefield both have 9-year-old architectural shingle roofs. A June storm with 72 mph straight-line winds moves through overnight. Both roofs lose ridge cap shingles and have lifted sections along the south-facing rake edge.

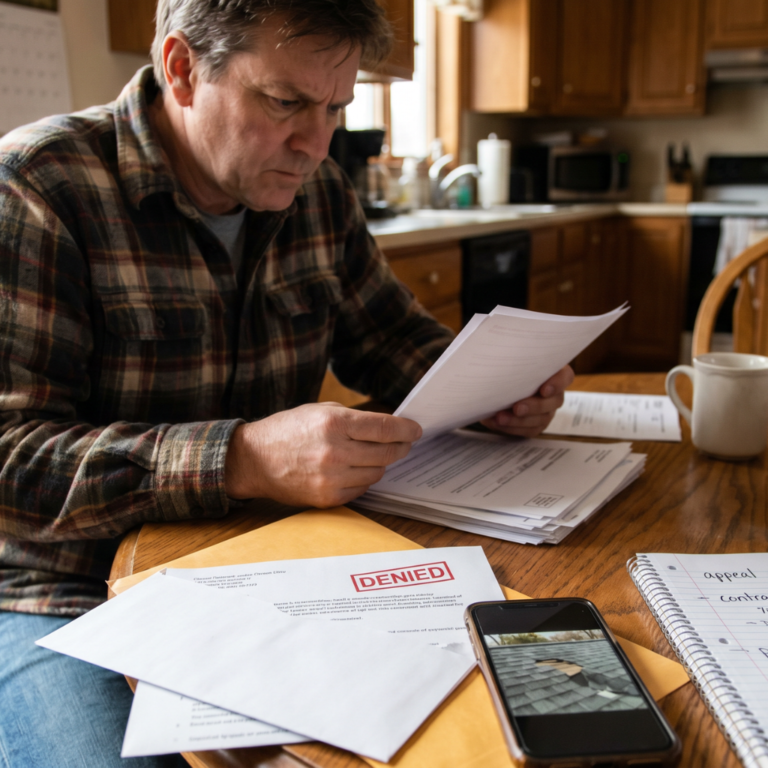

Homeowner A photographs the yard debris but not the roof, waits two weeks to call their insurer, and climbs on the roof, disturbing the damage pattern. The adjuster notes prior granule loss and calls it wear and tear. Claim denied.

Homeowner B calls a local contractor the next morning. The inspection documents lifted sealant bonds, exposed underlayment at the rake, and granule loss concentrated at impact points rather than uniform aging. The adjuster is present for the inspection. Claim approved for full roof replacement plus gutter resetting on the affected side. Same storm. Same neighborhood. Documentation and timing made all the difference.

Frequently Asked Questions

Q: Does homeowners insurance cover wind damage to my roof? A: Yes, if the damage is sudden and caused by the storm event. Standard policies cover wind as a named peril. Pre-existing wear and tear is not covered.

Q: What does wind damage look like on a roof? A: Missing shingles, lifted edges, broken sealant bonds, damaged ridge cap, granule loss in gutters, and damaged flashing. Damage is usually worst at edges, corners, and the ridge.

Q: What wind speed damages a roof? A: NWS Springfield defines damaging wind at 58 mph. Standard shingles are rated to 60 mph. Architectural shingles handle 110 mph. That gap explains why wind claims are so common here.

Q: Why was my wind damage claim denied? A: The four most common reasons are wear and tear, improper installation, lack of maintenance, and cosmetic damage exclusions. Documentation of the storm event and functional damage is the counter. Understanding how the claim process works helps you avoid these pitfalls.

Q: What is a cosmetic damage exclusion? A: A policy clause that excludes damage affecting only appearance, not function. If your roof still sheds water despite the damage, the insurer may call it cosmetic. Functional damage is still covered.

Q: How long do I have to file a wind damage claim in Missouri? A: No fixed statewide deadline. Your specific policy controls the timeline. File promptly using the storm date as the date of loss, not the day you notice the leak.

Q: Does wind damage cover more than the roof? A: Yes. Gutters, siding, soffit, and fascia damaged by the same storm belong on the same claim. Document all exterior surfaces before calling your insurer.

Q: How do I avoid storm chasers after a wind event? A: Watch for door-to-door crews, large upfront deposits, no local office, and pressure to sign immediately. Use a local contractor with a verifiable history in the area.

Key Takeaways

Wind in Springfield: June is the peak month for damaging wind. The 58 mph severe threshold is right at the limit of standard shingles. Architectural and Class 4 shingles offer meaningful upgrades.

Insurance Coverage: Standard policies cover sudden wind damage. The most common denial reasons are wear and tear and cosmetic exclusions. Check your declarations page for cosmetic exclusion language.

Document Everything: Photograph all exterior surfaces from the ground. Get a professional inspection before calling your insurer. Have your contractor present at the adjuster visit.

Full Exterior Claims: Wind damages more than the roof. Gutters, siding, and soffit from the same storm belong on the same claim.

Just Had Wind Come Through?

If your roof took a hit from a recent storm, get a professional out to document the damage before you call your insurer. That inspection is the foundation of a strong claim.

ProNail Exteriors offers free wind damage inspections across Springfield, Ozark, Nixa, Republic, Battlefield, Marshfield, and all of Southwest Missouri. In-house crews, full exterior documentation, and no pressure. Call (844) 321-6245.

ProNail Exteriors | Roofing, Siding, Windows, Gutters, Decks, and More | Serving Southwest Missouri Since 2025